Community currencies are based upon cohesion between their members and often aim to circumvent issues related to a lack of monetary supply, particularly within more marginalized populations. Based on trust and an aim to secure the local economy, it can be said that these currencies re-frame money as a constitutional project. However, many struggle to reach their goals. I will argue that a lack of capital and reliance on consumer transactions are their key challenges, and explore how debt and the generally inelastic need for housing security could be better leveraged by these communities.

Using the current socio-economic situation in Croatia as a case study, I will illustrate a speculative framework that would inject capital through collaboration with landlords. Croatia has a high home ownership rate, with many homeowners being older, working-class individuals who are approaching retirement age. Meanwhile, the younger generation struggles with high rent due to the growth of the tourism industry and owning a home has become an increasingly utopian ideal. Could an intergenerational dialogue provide some of the capital needed to secure the local economy and in turn, potentially slow down the brain drain to revitalize the local economy? This complementary currency would utilize housing as a universal need, and use debt to bind the different parties into a more stable, longer-term relationship.

Most complementary currencies, or community currencies, (CCs) tend to be small projects that aim to bolster the local community. Some, such as the Brixton Pound and the Berkshares, have met varying degrees of success within their localized goals. And yet many more struggle to scale-up towards their socio-political ambitions. Despite the relatively limited scope of CC projects today, the example of the WIR Franc demonstrates the potential for complementary currencies to play a larger socio-economic role. The WIR Franc Bank began in 1934 as a B2B (Business to Business) currency to facilitate trade between companies in times of monetary shortage. Today, the WIR Franc is worth close to 1% of the Swiss GDP. Beyond sheer financial worth, studies have more importantly shown that the WIR Franc has a counter-cyclical effect and helped businesses avoid economic downturn during times of financial crisis (Stodder & Lietaer, 2016).

As a B2B currency, the WIR Franc’s design is weighted by businesses’ velocity within their day-to-day trading. Most CCs today are targeted at individuals, creating a B2C (Business to Customer) or C2C (Customer to Customer) system. This creates a liquidity issue as the CC is largely dependent on a coincidence of wants and most are limited to being spent at shops. On examination of a typical household’s balance sheet, the most significant expenses are rarely at shops; in fact, one could argue that consumer level purchases are highly elastic. Furthermore, although perhaps less critically, this scheme is dependent on a consumerist culture, which such projects may often find themselves at ideological odds with. On the contrary, housing tends to be the largest and most inelastic expenditure across demographics, and yet this is not addressed in most CC schemes. Many CC schemes close their loop when participating shops redeem CC against the Euro or another currency within the CC-issuing organization. This makes the scheme dependent on the organization’s reserve of Euros, which is limited.

Keeping these weaknesses in mind, I propose structuring a currency design that targets these issues specifically, with the socio-economic challenges in Zagreb as a background.

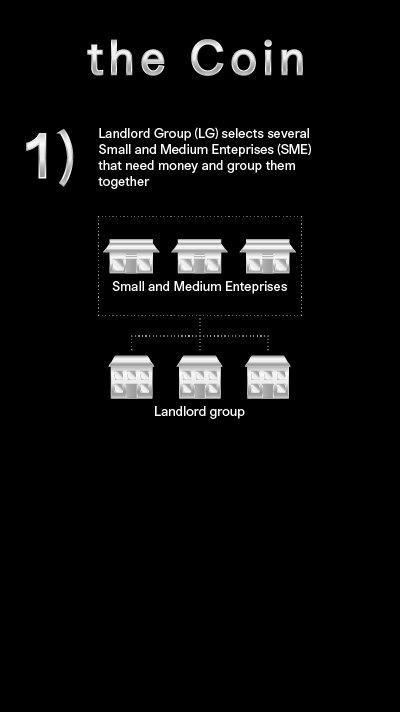

Croatia suffers from brain drain as many young and well-educated Croatians leave for Germany and the UK where there are better job prospects. While emigration has to a certain extent been happening for decades, it has become even more pressing with increased mobility through Croatia’s entry into the EU in 2013. Small and Medium Enterprises (SMEs) have a difficult time securing financing from traditional banking channels, further contributing to a lack of employment opportunities to retain talent. Rent is high in Zagreb, where residents have to compete against the tourism industry in the housing market and many struggle with the high costs of living in comparison to wages.

Similar to other countries in Central Europe, home ownership rate is high and owning a home has become a quasi-cultural expectation. Despite the high interest rates, many Croatians will buy a home from the moment they qualify for a mortgage because they see housing as a form of security into old age. As in many other places, the purchase of a home is rarely the most financially rewarding investment compared to other investment options available. Even with the acceptance of this financial paradox, securing a mortgage is not without obstacles. Mortgage qualification is dependent on a permanent job, which has become an increasingly rare phenomenon within an ever-pervasive and precarious global labour market.

Other demographics are equally strained. The elderly struggle with low pension payments and so often rent out their apartments to make ends meet. It is not uncommon to see older landlords owning multiple apartments while also remaining part of the working class. In Yugoslav times in the 70s, Croatia had socially owned, worker-managed enterprises, which also had housing for its employees. As the economy slumped, Yugoslavia took on loans with the IMF and an austerity programme was consequentially introduced. In the 1990s, as privatization began, these enterprise homes were sold mostly to the workers at below market prices. With the War for Independence (‘91-‘95), the state further sold off what was left of social housing at very low prices to raise funds quickly to finance the war. Thus today, many homeowners in Croatia of, or who are approaching, pension age are still part of the working class and defy the general Western idea that landlords are higher net worth individuals. This also means that as these landlords approach retirement age, they fear for their financial security as pensions are insufficient and the cost of living is rising.

My complementary currency scheme, called ‘the Coin’, aims to address the issues of SME financing, housing and the position of landlord-pensioners. Its principle aims are to fund local businesses to contribute to employment creation so that it is more attractive for young people to stay in Croatia, while also securing and providing relief in the housing rental market.

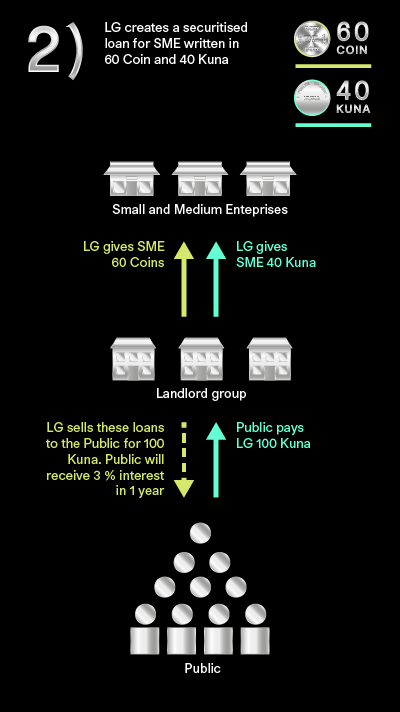

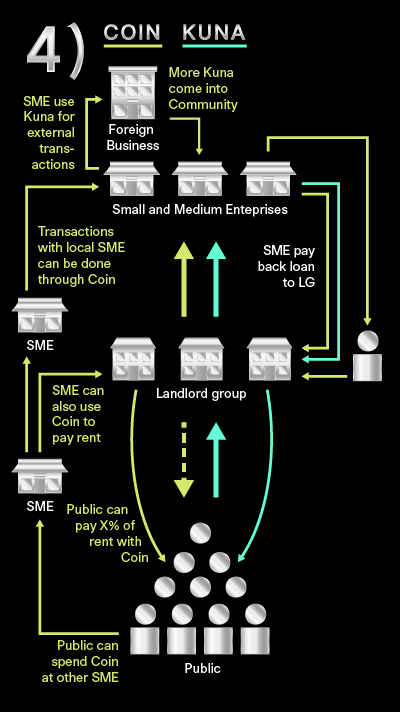

Structurally, where this Coin scheme differs from most CC projects is that the currency is based on a group of landlords – let’s call them Landlord’s Group (LG) – issuing a loan that is written in a mix of Coin and the Kuna, the fiat currency in Croatia. A fiat currency is the currency that is established by the government. Other examples of fiat currency include the Euro, the US dollar and the Japanese Yen.

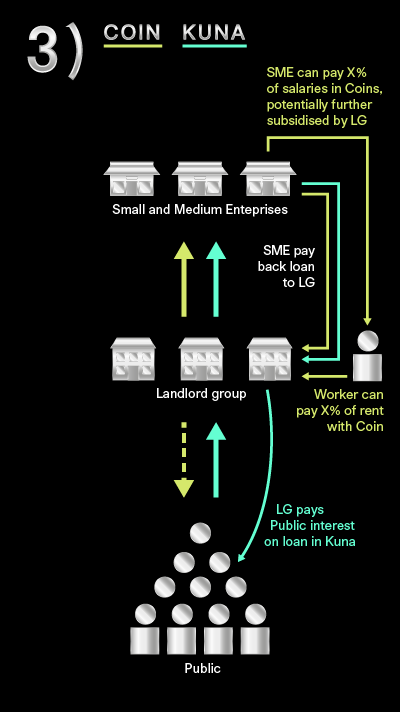

The loan is written in a mixture of Kuna and Coin so that both the SME and public can trade with the outside community whilst also using its maturity date to create a time-bound relationship with the local economy. It is unrealistic to assume that all of an individual’s needs are able to be satisfied through the local community alone. The loan’s writing in a mix of Kuna and Coin acknowledges this need for both. Similarly, the ability for SMEs to hold Kuna in addition to Coin is particularly important as the SMEs would otherwise lack the capital necessary to exploit opportunities outside of this immediate scheme to render them more competitive against globalized business chains that have already permeated the Croatian market. SMEs would then be able to use their reserves of Coin in local transactions as first resort and could also hire further employees with Coin. As an issuer of Coin with full monetary sovereignty over this community currency, it is further possible for LG to subsidize employment with further issuance of Coins. Coin can also be used among participating businesses in the local economy.

Most importantly, the Coin can be accepted for rent payments since landlords issued the Coin. This creates an immediate high use value for Coin holders. Since SMEs may also be renting from LG, they may also pay their rent through Coin.

It is possible to develop a similar theoretical scheme with a fiat currency not dissimilar to investment banks’ sales of bonds and commercial papers. However, requirements and transaction costs to bond issuance would be too forbidding for SMEs. More generally, the Coin aims to circumvent monetary limitations as a result of Croatia’s membership in the EU and plan to join the Eurozone. While Croatia currently operates in Kuna, its planned adoption of the Euro has meant that the exchange rate between the Kuna and Euro must be relatively stable. Moreover, there are specific limitations on the country’s budget and deficits, with deficit to GDP capped at 3%. The pressure to balance towards these targets has resulted in the government having less control over its monetary supply and less liberty to invest in its contracting economy. A complementary currency can potentially circumvent some of these limitations, successfully demonstrated by the WIR Franc historically.

A complementary currency can secure the local economy by encouraging commerce with local businesses. In its focus on domestic trade, the CC is a move away from an export-oriented economy, which has been argued to have a long-term negative effect on the economy. Resources directed towards export production means a reduction on resources allocated towards domestic needs. This creates a reliance on imports and the local economy becomes more vulnerable to external shocks, pressures and changes in exchange rates (Kaboub, 2007). Furthermore, a CC also provides monetary sovereignty to invest in the local economy such as in job creation, where the fiat currency, the Kuna in the case of Croatia, is restricted. Overall, this allows for more direct domestic investment and shifts away from dependency on foreign capital that comes with interest and often leads to a net resource transfer out of the country.

A fiat currency is fiat not because it is widely accepted by shops, but because one can pay taxes with the currency. Taxes legally define residency and draw the boundaries of a municipal or national community, no matter how imagined this community might be. My Coin proposal puts the role of landlords at centre-stage making them the issuer of both loans and Coin. This positioning emphasizes the home, the place of residence, as the definition of community. It is also designed to use housing to create an immediate use for Coin and to use housing as an alternative form of fiat, as housing is a universal need. This universal and largely inflexible need for housing becomes the connecting power that unifies Coin to the Community as a second order fiat, rather than by enforcing a tax on the Coin.

Taxation in situations where monetary sovereignty can be assumed, such as in the case of a Community Currency, is generally used as a measure against inflation when there is full employment. Social services can be funded through the issuance of more currency rather than through the collection of taxes. At 7.7% in 2018, Croatia’s unemployment rate is still above the EU average. Although Croatia has been experiencing a steady and significant drop in unemployment, this drop can largely be attributed to an exodus of younger Croatians to Germany and the UK in search of better job prospects, rather than an actual increase in employment (HINA, 2018; Vladisavljevic, 2019). Given that there is no full employment in Croatia, adding taxation in Coin would be an unnecessary intervention.

Meanwhile, given that rent is one of the largest expenses for most people, when Coin can be used towards meeting this expense, it would gain immediate and widespread currency by meeting this very significant need. This would also diffuse pressures in securing a wide range of businesses to participate in the scheme to create use value for Coin holders in the early adoption stage.

The question arises - why would a Croatian landlord take on the risks of such a venture, even speculatively? It is important to bear in mind that many Croatian landlords own multiple apartments because the government sold off social housing at unusually low prices to raise funds quickly. Thus, despite owning multiple assets, these landlords are generally not high net worth individuals. Many of these landlords are pensioners struggling to meet their daily expenses and are renting out their apartments to subsidize their income. Except in the case of death, selling the apartments is usually not considered an option because the interest rate offered for savings is near zero and these individuals generally don’t feel sufficiently well-informed about finance to invest that revenue elsewhere.

If this proposed loan scheme’s return is only higher than the inflation rate, then it would already be better than what long-term savings and government bonds currently offer and it would cover the landlord-pensioner’s expenses with inflation built in. Even though a conventional mutual fund portfolio may suggest a higher return, this proposal could address needs in a way that a conventional mutual fund cannot. Speaking with older people more generally, it is clear that once their living expenses are accounted for, what matters most to this population is their children and their future. Most would also prefer if their children lived closer to them instead of emigrating to other countries for work, and more often than not staying abroad for good. In addition to a crumbling pension system due to the lack of workers paying into the system and consequential government proposals to raise the retirement age, the mass emigration of young, well-educated Croatians is directly against their self-interests from a familial and emotional perspective. Therefore, a proposal that addresses both their financial and social needs can be at least as equally attractive as current investment options available to them via traditional retail banks.

My proposal is admittedly highly speculative. Specifically, it draws on existing social relationships and needs, attempting to leverage them in a risk-sharing, socio-financial network. Compared to more traditional financial or social projects, my proposal sees social and financial needs as interconnected, and tries to propel groups that lack financial capital into a position of socio-financial agency through the creation of debt instruments that bind the groups together over time. This stands in contrast to more traditional social projects that generally attempt to avoid debt. While debt has been and still is a burden on the working class, debt is also what is traded in financial markets to generate profit, most infamously highlighted in the example of the subprime mortgage crisis in 2007- 08. Mortgages, loans, consumer and other household debt continue to be traded on credit markets today, and lead to what can be decades long of debt service on the households’ part, providing steady fuel to financial markets. In binding SMEs, landlords and the public together via a loan, it is in all parties’ interests for the SMEs to succeed, as the Loan pays a dividend. It is also in all parties’ interests for the Coin to succeed, as the Loan is written in both fiat currency and Coin. Instead of ignoring debt, through sharing both the risk and benefits of debt, this proposal tries to make the working class the direct owners and beneficiaries of debt-as-asset, a position that is normally only occupied by financiers, and to become a force of negotiation in finance, rather than remaining in the service of debt.

One could say that I am proposing that we financialize the social, which may be especially controversial at a time where big data and the sharing economy are rightly under critique for attempting to reduce human interactions to mere financial values. Additionally, my proposal still has many unanswered questions, such as how to keep the group of landlords’ power in check and will require further attention in many details.

However, once we begin to move beyond fiat currencies, it becomes clearer that we can also approach money as an abstract expression of cultural values and priorities. Amidst growing economic qualities, and where finance – the management of money - seems to be a driver of these inequalities and irresponsive to social needs, questions concerning how finance can relate back to the social have become increasingly relevant. Instead of financializing the social, through my hyper-speculative scheme, I propose that we attempt to socialize finance. Whereas most transactions today are rooted in a financial logic as the lowest common denominator, my speculation aims to position social needs as the underlying rational in financial organization.

HINA, (2018) More than 47,000 People Left Croatia in 2017. Available at: https://www.total-croatia-news.com/politics/29920-more-than-47-000-people-left-croatia-in-2017 Accessed 1 March 2019

Kaboub, F. (2007) ELR-led Economic Development: A Plan for Tunisia, The Levy Economics Institute of Bard College, Working Paper No. 499, May/ Available at: http://www.levy.org/pubs/wp_499.pdf Accessed 3 March 2019

Stodder, J. and Lietaer, B. (2016) The Macro-Stability of Swiss WIR-Bank Credits: Balance, Velocity, and Leverage Comp Econ Stud 58: 570.

Vladisavljevic, A. (2019) One-Way Ticket: Croatia’s Growing Emigration Crisis, Balkan Insight, Available at: https://balkaninsight.com/2019/01/08/one-way-ticket-croatia-s-growing-emigration-crisis-12-21-2018/ 8 January. Accessed 1 March 2019